What is Disability Insurance?

Disability Insurance is coverage designed to protect your income in the event you are no longer able to work due to an injury or illness. An insurance policy is issued for a set amount based on your income. In the event that you were to become disabled, the policy would pay a set benefit amount (typically on a monthly basis) which can be used to pay for monthly bills such as your mortgage, car payments and other living expenses.When do benefits start?

Disability Insurance policies include an Elimination Period. This is the period of time between when your are unable to work due to a disability and the benefits begin paying. Typically a long term disability policy will have an elimination period of 90 or 180 days. When you are applying for disability coverage, you will elect the elimination period that makes the most sense for your own personal situation. As a general rule of thumb, the shorter the elimination period, the higher the premium will be.How long will the benefit pay?

The majority of Long Term Disability policies are designed to pay through retirement or to age 65, however carriers will offer a benefit period for as little as 2 years.Why do I need Disability Insurance?

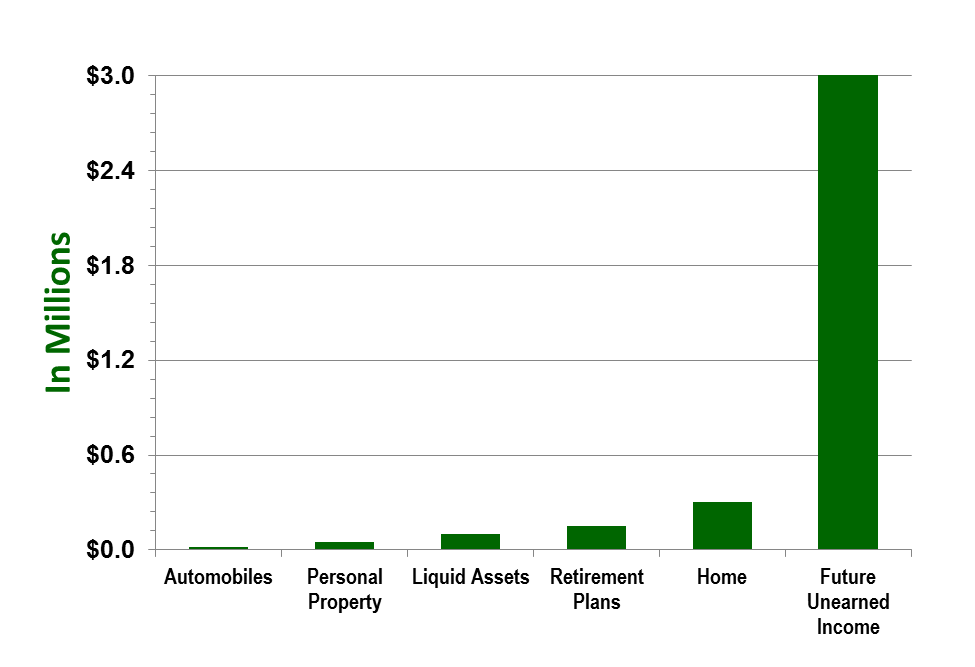

For most working Americans, our ability to earn an income is our greatest asset. Without an income, how would you pay for your monthly liabilities? Save for retirement? Or your children’s education? The chart below illustrates the value of income over time.

Assumption: 35 year old earning $100,000 annually